Pension Gap

RIVERSIDE (CNS) – The Board of Supervisors signed off on a report Tuesday showing that the Riverside County government’s unfunded pension liabilities are now close to $4 billion, up more than a half-billion dollars in the last two years, though projections are for the pension gap to narrow over the coming decade.

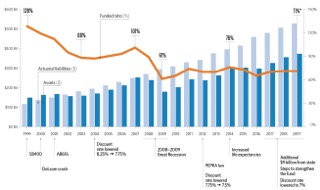

According to the 2025 Pension Advisory Review Committee report, the county’s retirement apparatus is now 75% funded, compared to 75.3% previously. The key metric reflective of a sound pension system is considered 80% funded status.

The county’s total unfunded pension gap is $3.94 billion, compared to $3.67 billion estimated in the 2024 report, PARC officials said.

“Based upon several factors, the long-term pension outlook remains favorable, with increases projected to peak early in the next decade,” the report stated. “The funded status is anticipated to be more than 80% within ten years, which has suffered a setback due to the negative investment returns experienced in fiscal year 2021-22. Projections will be tempered by year-to- year financial market performance.”

“You’re never going to meet the minimum standard,” Roy Bleckert of Moreno Valley told the board. “No matter how hard you try to pedal that bicycle, the expenses just keep outpacing income. We’ve been hearing for decades about how you’re moving money. But it’s like trying to grab the last deck chair on the Titanic before it slips underwater. You never get to the point where you’re above water.”

There are two main categories in the local pension system — safety and miscellaneous. The safety category covers sheriff’s deputies, District Attorney’s Office investigators, probation agents, and others, while the miscellaneous rolls cover clerks, custodians, nurses, social workers, technicians, and remaining employees not involved in any law enforcement function.

Poor investment returns going back to the Great Recession have required the county to pay higher amounts to CalPERS to cover loses in the safety and miscellaneous categories.

Employees across the spectrum in county government generally contribute less than 10% of gross earnings toward their defined-benefit plans with CalPERS.

General fund allocations to support the retirement system will steadily rise over the next decade, approaching $900 million in support by the mid 2030s, according to PARC.

Despite the big outlays, Supervisor Chuck Washington said the county continues “to be assertive in shoring up our finances,” to which board Chairman Manuel Perez added, “We’re in a better position now than we were before.”

The county gained some near-term relief from higher pension costs by selling $716 million in bonds at low interest rates in May 2020 and applying the proceeds to pension debt reduction, or what then-Supervisor Kevin Jeffries compared at the time to “using a credit card to pay off a credit card.”

In the past, Jeffries and other supervisors had expressed a desire for the county to phase out some defined-benefit plans in favor of defined- contribution plans, in line with most private sector retirement guarantees. Executive Office staff described the process as riddled with hurdles because of requirements in state law.

Beginning in September 2012, new hires in the safety category began accruing retirement benefits under a 2% at 50 formula, while newly hired miscellaneous workers began accruing benefits under a 2% at 60 formula.

For more Riverside County News Visit www.zapinin.com